Veriphy’s AML Guidance for a PEP

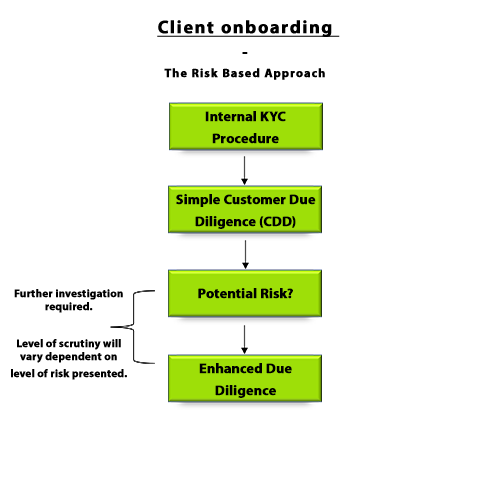

Step 1: Determine if a customer is a PEP

Businesses are not required to perform extensive investigations to determine if an individual is a PEP. Rather, this can be achieved via a simple AML check which includes a screen against a register of publicly known individuals with public functions, their associates and close family.

It is important to note that, inevitably, many PEP matches are false positives. This is due to the absence of information such as date of birth relating to actual PEPs.

Step 2: Enhanced Due Diligence

In the event of a client flagging against the PEP list, the relevant person within the organization must revert to their business’s internal KYC and onboarding procedures. Regulated firms should have individual policies and procedures for clients who during the onboarding process, flag up as high-risk.

Enhanced due diligence simply means the collection of additional data on an individual in order to mitigate risk.

Practical examples include:

- Establishing source of funds and wealth

- Enhanced monitoring of transactions

- Carrying out additional searches on the individual (such as an adverse media check)

- Establishing the intended purpose and nature of the business relationship

Step 3: Periodical Reviews

A potential high-risk client will need to be regularly monitored. Most financial organizations have in place systems which monitor for PEPs. This essentially involves screening the individual against the PEP register.

This may be done as part of your annual client base check.

Veriphy also offers a PEP Alert service available on a weekly or monthly basis to ensure your firm always remains compliant.